ChatGPT, a revolutionary AI-based conversational chatbot, has been making headlines around the world. The AI-based tool can answer user queries and generate new content in a human-like way. By automating tasks such as customer support and content creation, ChatGPT has the potential to revolutionize many industries, resulting in a more efficient digital landscape and an enhanced user experience. However, the technology is not without its risks and poses a number of issues, such as creating malicious content, copyright infringement, and other moral issues. Despite these challenges, the possibilities for ChatGPT are infinite, and with the advancement of technology, the opportunities it presents will only continue to expand.

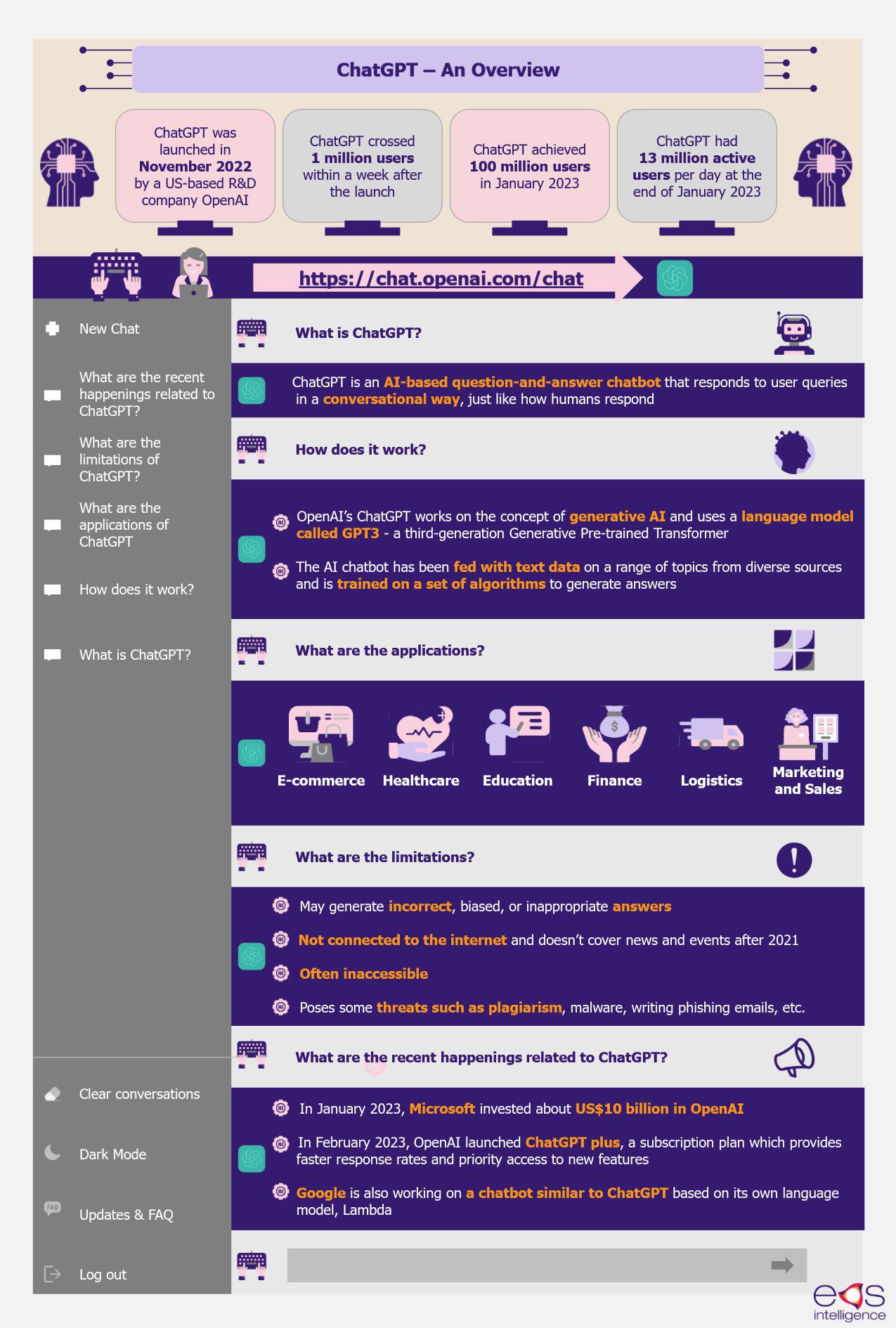

ChatGPT is an AI-based question-and-answer chatbot that responds to user queries in a conversational way, just like how humans respond. OpenAI, a US-based research and development company, launched ChatGPT in November 2022. Since then, ChatGPT has garnered increased attention and popularity worldwide. The tool surpassed over 1 million users within five days and 100 million users within two months of launch.

ChatGPT has become popular due to its capability to answer queries in a simple and conversational manner. The tool can perform various functions, such as generating content for marketing campaigns, writing emails, blogs, and essays, debugging code, and even solving mathematics questions.

OpenAI’s ChatGPT works on the concept of generative AI and uses a language model called GPT3 – a third-generation Generative Pre-trained Transformer. The AI chatbot has been fed with about 45 terabytes of text data on a diverse range of topics from sources such as books, websites, and articles and has been trained on a set of algorithms to understand relationships between words and phrases and how it is used in context. This way, the model is able to develop an understanding of languages and generate answers. ChatGPT uses a dialog format, asks follow-up questions for clarification, admits mistakes, and is capable of dismissing inappropriate or dangerous requests.

ChatGPT also has a simple user interface, allowing communication through a plain textbox just like a messaging app, thus making it easy to use. Currently, ChatGPT is in beta testing, and users can use it for free to try and provide feedback. However, the free version is often inaccessible and out of capacity due to the increasing traffic.

In February 2023, OpenAI launched a pilot subscription plan named ChatGPT Plus, starting at US$20 per month, which is available to its customers in the USA. The subscription plan provides access to ChatGPT even during peak times and provides prior access to any new features. OpenAI is also testing ChatGPT to generate videos and pictures using its DALLE image-generating software, which is another AI tool developed by OpenAI to create art and images from text prompts. OpenAI also plans to launch a ChatGPT mobile app soon.

How could ChatGPT help businesses?

One of the most impactful areas where ChatGPT can make a difference is customer support. The AI tool can handle a large volume of consumer queries within a short time frame and give accurate responses, which can boost work efficiency and reduce employees’ workload.

In addition, the tool can also be employed to answer sales-related queries. By training ChatGPT to understand product information, pricing, and other details, businesses can provide a seamless sales experience for customers. ChatGPT can also analyze user data and behavior and can assist customers to find the products they are looking for, and give product recommendations leading to a more tailored and enjoyable shopping experience. ChatGPT can be incorporated into websites to engage visitors and help them find the information they need, which can help in lead generation.

Another potential benefit of ChatGPT is its ability to automate content generation. ChatGPT can generate unique and original content quickly, making it an effective tool for creating marketing materials such as email campaigns, blogs, newsletters, etc.

ChatGPT could be used in a number of industries, such as travel, education, real estate, healthcare, information technology, etc. For instance, in the tech industry, ChatGPT can write programs in specific programming languages such as JavaScript, Python, and React, and can be very helpful to developers in generating code snippets and for code debugging.

In healthcare, the tool can be used in scheduling appointments, summarizing patient’s health information based on previous history, assisting in diagnostics, and for telemedicine services.

In the education sector, ChatGPT can be used to prepare teaching materials and lessons and to provide personalized tutoring classes.

These are just a few applications of ChatGPT. As generative technology continues to evolve, there may be many other potential applications that can help businesses achieve their goals more efficiently and effectively.

Is ChatGPT Just Another Tech Innovation or A Game Changer by EOS Intelligence

ChatGPT’s output may not be always accurate

While ChatGPT offers several benefits and advantages, the tool is not without limitations. ChatGPT works on pre-trained data that cannot handle nuances or other ambiguities and thus may generate answers that are incorrect, biased, or inappropriate.

Moreover, ChatGPT is not connected to the internet and cannot refer to an external link to respond to queries that are not part of its training. It also does not cover the news and events after 2021 and cannot provide real-time information.

Another major limitation is that the tool is often out of capacity due to the high traffic, which makes it inaccessible. There are also other potential risks associated with these generative AI tools. Some of the threats include writing phishing emails, copyright infringement, generating abusive content or malicious software, plagiarism, and much more.

ChatGPT is not the first or only AI chatbot

While ChatGPT has garnered most of the attention in the last few months, it is neither the first nor the only AI-based chatbot in the market. There are many AI-based writers and AI chatbots in the market. These tools vary in their applications and have their own strengths and weaknesses.

For instance, ChatSonic, first released in 2020, is an AI writing assistant touted as the top ChatGPT alternative. This AI chatbot is supported by Google, has voice dictation capabilities, can generate up-to-date content, and can also generate images based on text prompts. However, ChatSonic has word limits in its free as well as paid versions, which makes it difficult for users who need to generate large pieces of text.

Similarly, Jasper is another AI tool launched in 2021, which works based on the language model (GPT-3) similar to ChatGPT. Jasper can write and generate content for blogs, videos, Twitter threads, etc., in over 50 language templates and can also check for grammar and plagiarism. Jasper AI is specifically built for dealing with business use cases and is also faster and more efficient and generates more accurate results than ChatGPT.

YouChat is another example, developed in 2022 by You.com, and running on OpenAI GPT-3. It performs similar functions as ChatGPT – responding to queries, solving math equations, coding, translating, and writing content. This chatbot cites source links of the information and acts more like an AI-powered search engine. However, YouChat lacks an aesthetic appeal and may generate results that are outdated at times.

ChatGPT-styled chatbots to power search engines

While a lot of buzz has been created about this technology, the impact of AI-based conversational chatbots is yet to be seen on a large scale. Many proclaim that tools such as ChatGPT will replace the traditional search method of using Google to obtain information.

However, experts argue that it is highly unlikely. While AI chatbots can mimic human-like conversation, they need to be trained on massive amounts of data to generate any kind of answers. These tools work on pre-trained models that were fed with large amounts of data sourced from books, articles, websites, and many more resources to generate content. Hence, real-time learning and answering would be cost-intensive in the long run.

Moreover, ChatGPT’s answers may not always be comprehensive or accurate, requiring human supervision. ChatGPT may also not be very good at solving logical questions. For instance, when asked to solve a simple problem – “RQP, ONM, _, IHG, FED, find the missing letters”, ChatGPT answered incorrectly as “LKI”. Similarly, when provided a text prompt, “The odd numbers in the group 17, 32, 3, 15, 82, 9, 1 add up to an even number”, the chatbot affirmed it, which is false. Moreover, the AI chatbot does not cover news after 2021, and when asked, “Who won the 2022 World Cup?” ChatGPT said the event has not taken place.

On the other hand, Google uses several algorithms to rank web pages and gives the most relevant web results and comprehensive information. Google has access to a much larger pool of data and the ability to analyze it in real time. Additionally, Google’s ranking algorithms have been developed over years of research and refinement, making them incredibly efficient and effective at delivering high-quality results. Therefore, while AI chatbots can be useful in certain contexts, they are unlikely to replace traditional search methods, such as Google.

However, leading search engines are looking to incorporate ChatGPT into their search tools. For instance, Microsoft is planning to incorporate ChatGPT 4, a faster version of the current ChatGPT version, into its Bing Search engine. Since 2019, the company has invested about US$13 billion in OpenAI, the parent company of ChatGPT.

In February 2023, Microsoft also incorporated ChatGPT into its popular office software Teams. With this, users with Teams premium accounts will able to generate meeting notes, access recommended tasks, and would be able to see personalized highlights of the meeting using ChatGPT. These add immense value to the user.

In February 2023, China-based e-commerce company Alibaba also announced its plan to launch its own AI chatbot similar to ChatGPT. Similarly, Baidu, a China-based internet service provider, launched a chatbot named “Ernie” in its search engine in March 2023.

Amidst the increasing popularity of ChatGPT, Google has also started working on a chatbot named “Bard” based on its own language model, Lambda. The company is planning to launch more than 20 new AI-based products in 2023. In February 2023, Google invested about US$400 million in Anthropic AI, a US-based artificial intelligence startup, which is testing a new chatbot named Claude. Thus, the race to build an effective AI-enabled search engine has just begun, and things have to unfold a bit to learn more about how chatbots can modify web searches.

On the other hand, AI technologies such as ChatGPT are sure to leave an impact on how businesses operate. With the global economy slowing down, resulting in low business margins, many businesses are looking to cut down costs to increase profitability.

ChatGPT could be extremely beneficial to companies looking to automate various business tasks, such as customer support and content generation. The tool can be integrated into channels, including websites and voice assistants. While this sounds beneficial, there is also a likelihood of the technology displacing some jobs such as customer service representatives, copywriters, research analysts, etc.

However, ChatGPT will not be replacing the human workforce completely since many business tasks require creative and critical thinking skills and other traits such as empathy and emotional intelligence that only humans have. This technology is expected to pave the way for new opportunities in various fields, such as software engineering and data analysis, and allow employees to focus on more value-added tasks instead of routine, mundane tasks, ultimately boosting productivity.

EOS Perspective

With their remarkable ability to generate human-like conversations and high-quality content, generative AI tools, such as ChatGPT, are sure to be touted as a game-changer for many businesses. The advancements in generative AI are expected to have a significant impact on various business tasks such as customer support, content creation, data analysis, marketing and sales, and even decision-making.

Investors are slowly taking note of the immense potential the technology holds. It is estimated that generative AI start-ups received equity funding totaling about US$2.6 billion across 110 deals in 2022, which echoes an increasing interest in the technology.

The adoption of generative AI technologies is poised to increase, especially in business processes where a human-like conversation is desirable. Industries such as e-commerce, retail, and travel are likely to embrace this technology to automate customer service tasks, reduce costs, and increase efficiency. In addition, generative AI is likely to become an indispensable part of industries such as finance and logistics, where high levels of accuracy and precision are required. Media and entertainment companies can also benefit from this technology to quickly generate content such as articles, videos, and audio.

That being said, generative AI is not without its risks, and the technology could be used to create fake and other discriminatory information. Hence, there is an inevitable need to ensure that generative AI models are trained and deployed in an ethical and responsible manner. Despite these challenges, there is increased research and significant activity going on in the field of generative AI, especially with regard to combining the capabilities of chatbots and traditional search engines.

The current chatbots will continue to evolve and will lead to the creation of even more advanced and sophisticated models. The popularity of generative AI tools such as ChatGPT is unlikely to wane, and the technology is here to stay, with the potential to create better prospects for business and a brighter future for society.