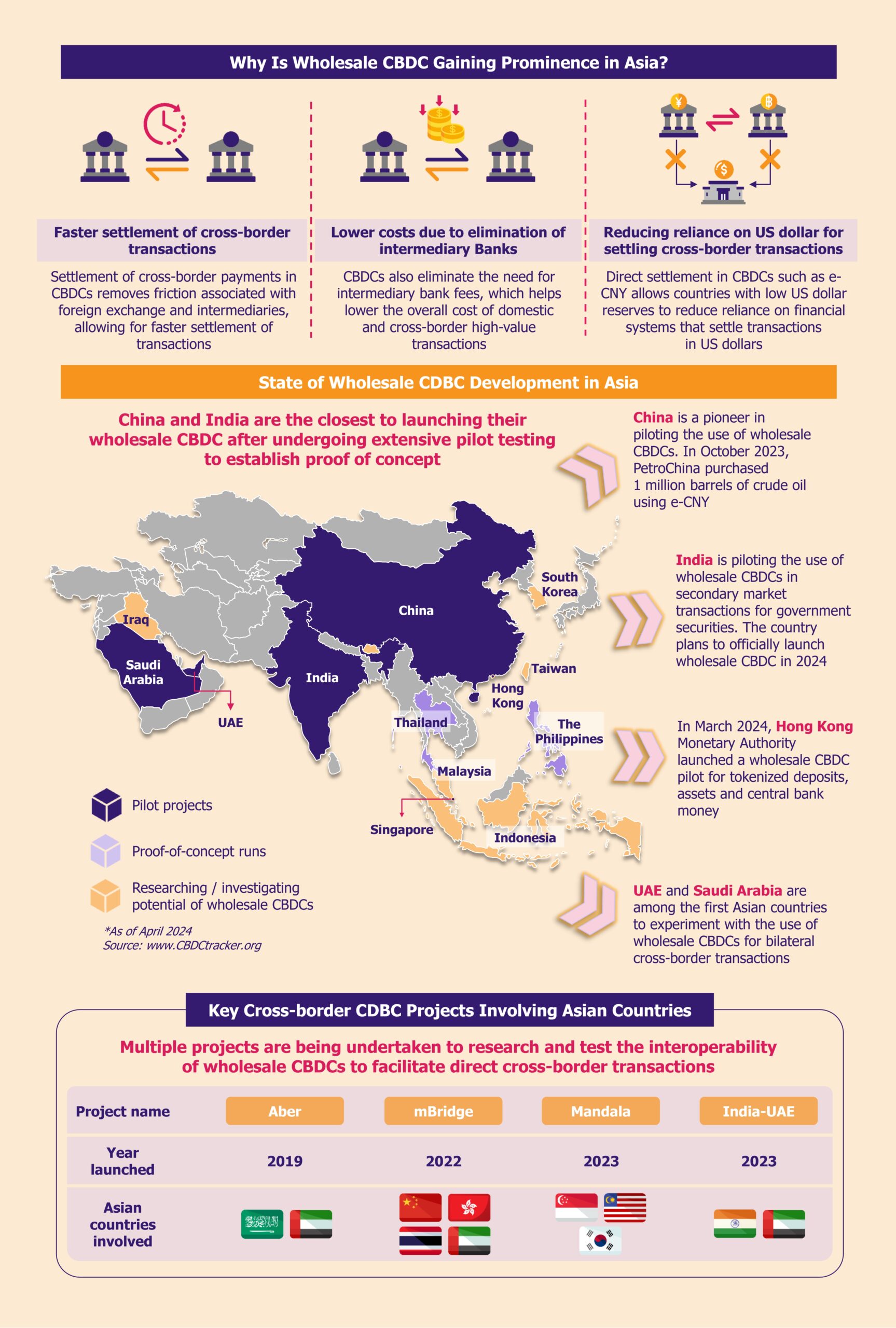

Sweden’s cashless initiative is gaining momentum, driven by high digital literacy, favorable regulations, and rapid adoption of technology. Since most consumers (~95%) are digitally savvy, a tendency to prefer mobile payments over cash is pushing Sweden closer to its goal of becoming a cashless economy. Technology solutions will likely play a crucial role in shaping the evolution of payment systems as Sweden transitions to a cashless society.

Consumer preference for mobile payments drives Sweden’s cashless shift

The shift toward a cashless society in Sweden reflects both consumer preferences and the increasing number of businesses that prefer or require card and mobile payments. At the same time, Swedish society shows a high level of trust in banks and government institutions, which reduces resistance to financial innovation. Together, these factors create a strong foundation for the widespread adoption of new digital payment systems.

Since the COVID-19 pandemic began in early 2020, cash usage has declined, with cash in circulation accounting for only 1% of the country’s GDP, owing to the convenience and security of digital transactions.

Card offerings, such as Handelsbanken’s Allkort Mastercard, SAS EuroBonus Cards, and the Lunar-SAS partnership, encourage consumers to adopt digital payments by offering various reward programs, including cashback, bonus points, and travel incentives.

Growth in real-time payments fast-tracks the cashless initiative

The Swish mobile payment system is boosting the country’s cash-free initiative by driving growth in real-time payments. Swish is the country’s second most common payment method, highlighting its significance in Sweden’s digital payment landscape. A recent addition of the tap-to-pay function in December 2024 has further expanded Swish’s capabilities for in-store purchases for over 8.6 million Swedish app users (a high number, considering the country’s population is around 10.5 million).

Moreover, the Riksbank, Sweden’s central bank, intends to expand its RIX-INST, a real-time settlement service that currently only allows for domestic payments. The government plans to explore synergies between the RIX INST system and other regional systems, such as the European Central Bank, Banca d’Italia, and Danmarks Nationalbank, seeking to facilitate cross-border payments utilizing cross-currencies. The plan focuses on supporting seamless international transactions that would ultimately strengthen Sweden’s position as a global leader in digital payments.

Despite this favorable scenario for Sweden’s cashless initiative, Sweden’s central bank still aims to support both cash and digital payments, as a way to be more inclusive. This means that while digital payments will continue to be a popular option, cash payments should not disappear entirely. Swedish authorities acknowledge that the role of cash is still key, especially to protect vulnerable groups such as the elderly population and people with disabilities. In case of emergencies (natural disasters, cyberattacks, or other crises where digital systems might fail), cash will also be necessary.

Cashless Sweden: Prepared or Vulnerable? by EOS Intelligence

Open-banking regulations aid in alternative payment adoption

In 2019, Sweden implemented the EU’s revised Payment Services Directive 2 (PSD2). This European law aims to strengthen customer authentication, ensure proper authorization and regulation of third-party providers, enhance security and data protection, and promote open banking.

The ratification of the recent revision to PSD2 fosters growth in open banking in Sweden, resulting in innovative fintech products such as digital identity BankID. This innovative system leverages secure certificates and biometric authentication to enhance security. Users across Sweden rely on this innovative system for secure authentication and digital signatures.

The adoption of open banking greatly benefits Sweden’s cashless initiative. Companies such as the Swedish payment platform Open Payments enable real-time payments directly from consumers’ bank accounts and facilitate seamless bank-to-bank transfers without intermediaries. These capabilities are accelerating the growth of account-to-account (A2A) payments and solidifying the foundations of a cashless economy.

Government plans new regulations to improve consumer protection

Alternative payment methods (APMs) such as Buy Now Pay Later (BNPL or simply Pay Later) have become essential to Sweden’s cashless success. Klarna has emerged as the leading provider of BNPL solutions, with other players, including Walley, Qliro, and Zaver, also growing their presence. BNPL’s seamless integration with all major e-commerce platforms, technology partners, and payment service providers (PSPs) enhances its accessibility and adoption.

Regulators plan to fully implement the updated regulation, the Consumer Credit Directive 2 (CCD2), by Q4 2026, aiming to make APMs even more accessible and safer for consumers. Under the directive, APM providers must conduct in-depth assessments of credit liability to ensure responsible lending, expand coverage of interest-free loans under €200, and comply with clearer advertising rules that include mandatory warnings when consumers take on debt.

AI and Blockchain facilitate secure and automated transactions

Tapping into the growing prevalence of cryptocurrency, the Riksbank has been exploring the development of its digital currency, e-Krona, based on distributed ledger technology (DLT), which offers a more secure digital payment method.

The Riksbank launched several pilot programs between 2021 and 2024 to explore the application of e-Krona in both retail and wholesale transaction setups. The bank expects this token-based, state-backed digital currency to complement existing payment systems and enhance financial stability. It also aims to promote greater inclusivity by acting as a public alternative to cash.

Technology is also driving a change in consumer preference for digital payments. The growing integration of IoT and AI enables seamless and automated transactions, further accelerating the country’s transition to a cashless society.

Although the vast majority of payments in Sweden are already digital, there is no precise data on how often consumers use voice‑activated transactions via Google Home, Alexa, or similar platforms. The rapid integration of payment apps with these connected devices suggests a strong likelihood that voice-activated and IoT-based payment solutions will gain traction in the future.

Added compliance and limited infrastructure access challenge fintechs

Lack of access to central financial infrastructure is a significant challenge for most fintech companies, forcing them to rely on banks and other intermediaries to provide essential financial services. This results in higher costs, reduced efficiency, and a limited ability to compete with traditional financial institutions.

Infrastructure upgrade and scalability

The Riksbank is looking to modernize the payments infrastructure to facilitate the integration of more fintech companies with its RIX payment system. This modernization aims to support the growing number of fintech companies adopting new cashless payment technologies while ensuring the stability and resilience of Sweden’s payment infrastructure.

e-Krona, albeit still in its pilot phase, presents a transformative initiative. However, the government must ensure scalability for successful widespread adoption among merchants. Processing a large volume of transactions without compromising speed or security remains a significant hurdle. Moreover, e-Krona must seamlessly integrate with Sweden’s payment systems, such as Swish.

Regulatory compliance

Fintech companies seeking to enter Sweden often find it difficult to navigate the complex regulatory landscape set by the Swedish Financial Supervisory Authority (Finansinspektionen). According to a survey by SweFinTech, an independent financial association, 82% of its fintech members reported being weighed down by the additional burden of anti-money laundering and combating the financing of terrorism (AML/CTF) regulations. Companies are increasingly implementing Regulatory Technology (RegTech) solutions to monitor transactions, ensure data integrity, and comply with Sweden’s national and international regulations.

As digital payments increase, merchants must also invest in cybersecurity measures against rising threats. This compounds costs due to high interchange fees, ultimately reducing profit margins.

Potential disruptions and cyberattacks

Disruptions and cyber risks regarding the country’s payment network are also a concern, prompting a cautious approach. Between 2023 and 2024, brief outages disrupted critical digital payment infrastructure, affecting the Riksbank’s RIX system and the supporting systems for Swish, including Bankgirot, Getswish AB (Swish), and BankID.

In these cases, the disruption did not cause major issues. However, with growing concerns about cyberattacks amid Europe’s uncertain geopolitical climate, Sweden is taking steps to protect its cashless economy. To reduce the impact of possible outages, the Riksbank is considering a system that would allow offline card payments for essential goods during disruptions lasting up to seven days.

The Swedish government has also encouraged people to keep enough cash on hand to cover a week’s worth of necessities, helping households stay prepared in case of a cyberattack.

EOS Perspective

Sweden’s swift move towards becoming cashless reflects the country’s focus on digitalization, innovation in fintech, and regulatory changes. The growing adoption of platforms such as Swish and Klarna suggests that Swedish consumers are highly tech-savvy, regardless of age. This trend also indicates that flexible payment solutions can drive consumer behavior to prefer digital payment methods over cash.

The integration of blockchain and IoT technologies into payment systems is likely to offer new opportunities in improving the efficiency and security of digital transactions, reinforcing Sweden’s position as a global leader in cash-free transactions.

There is significant room for developing and launching innovative financial tools and services, offering opportunities for fintech companies. Real-time payment innovations, such as Swish, and blockchain-based solutions that benefit from the rise of decentralized finance (DeFi) offer promising growth opportunities. RegTech tools that improve digital identity verification, AML compliance, and AI-driven financial planning tools may also witness growth.

Sweden’s strict regulatory and compliance requirements, as well as the difficulty of obtaining access to central financial infrastructure controlled by established banks, remain challenging, particularly for fintech companies attempting to enter the market. Arbitrary de-risking by banks, which has affected nearly 40% of fintech companies in 2023 by restricting banking services, further challenges companies.

Nonetheless, open-banking initiatives that grant access to third-party providers suggest a shift toward a more inclusive economy, enabling greater competition, easier market entry for fintech companies, and broader access to digital payment solutions for both consumers and businesses.

Further enhancements in financial infrastructure will support a cashless economy. Modernization of the Riksbank’s RIX payment system will enable more fintech companies to participate, while also facilitating integration into Sweden’s payment system.

The potential introduction of e-Krona offers further opportunities to increase inclusivity, which in turn boosts cashless adoption. However, we must wait and see how it evolves as the Riksbank continues to monitor the development of other digital currencies, such as the Digital Euro.

While Sweden has made significant strides toward its cashless vision, progress may stall due to Europe’s current scenario, amid a vulnerable political environment and the risk of susceptibility to cyberattacks. Nevertheless, the country has demonstrated a clear trend toward becoming a digital-first economy, evident in its low reliance on cash usage and the ongoing development of a robust digital payment infrastructure.